The question of "Is it a good time to buy a house?" yields a different answer for everyone. Real estate is as personalized as taxes, though the headlines and guidance like to make it seem like it's a one size fits all answer.

In this post, we will break down how to determine if buying a home makes sense for you. We will identify the factors to consider, and how to do the math so that you know how to make a decision based on your specific situation. We'll even discuss how to analyze a specific property or properties. Let's get started!

Key Performance Indicators

From a financial perspective, there are several Key Performance Indicators that can help you determine if it’s a good time to buy a house:

You will live in the home long enough to earn a net profit (Total appreciation > Total cost of ownership).

You have enough of a down payment that allows you to have a net profit within the time horizon that you plan on keeping the home.

You have a low enough interest rate that allows you to have a net profit within the time horizon that you plan on keeping the home.

The outcomes above should not be discarded as guaranteed or obvious. While 90% of home owners sell for more than what they bought for, up to 60% lose money due to the cost of ownership exceeding how much the home went up in value (Net Loss).

Aligre Insight: A home can go up in value and you'll still lose money simply because the amount of money you spent owning the home was more than it went up in value.

This includes money spent on interest, property taxes, insurance, utilities, repairs and maintenance.

Appreciation vs Cost of Ownership

To illustrate how interest payments and property taxes often outrun appreciation, here is an example that shows how many years of ownership it takes for annual appreciation to outpace annual expenses, and most importantly how long it takes for the average American home to produce a net profit (good investment). We will explore a scenario based on the following assumptions:

Home price: ~$400,000

Down Payment: 20%

Interest Rate: 6.3%

Property Tax Rate: 1% property tax rate

Insurance Rate: 0.5%

Annual Utilities: $4,800

Annual Maintenance & Repairs 1.5%

Annual Appreciation ~4-5%)

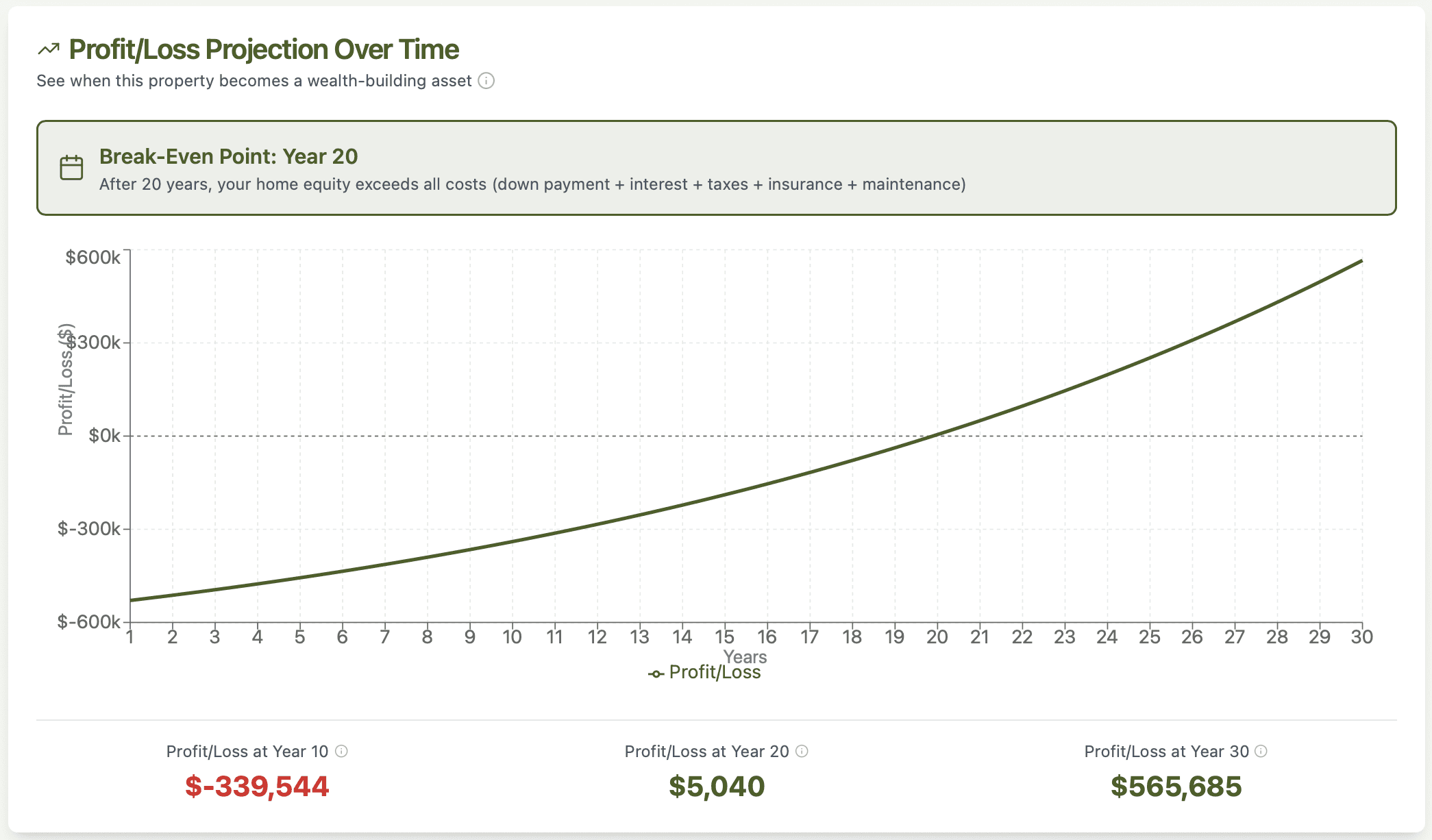

In this scenario, cost of ownership exceeds appreciation amounts for the first 20 years of ownership.

Aligre Insight: It would take 20+ years before a home bought under these circumstances actually results in the home owner gaining wealth. This is because mortgage interest is high in the early years, but decreases over time as principal is paid down, while appreciation compounds on the home's growing value (which also increases property taxes). The exact timing depends on local factors and appreciation rates: higher appreciation (e.g., 5%+) shortens it to ~19 years, while lower rates (e.g., 4%) push it to ~27 years.

Net Profit (Good Investment)

In the scenario above, Net Profit will occur after 20+ years of ownership. This accounts for total carrying costs (interest + taxes + insurance + utilities + maintenance/repairs), initial down payment, and selling costs (~7% of sale price for commissions and fees). Profit = (sale price - purchase price) - selling costs - cumulative carrying costs.

The real kicker? Even if you sell your home at a net loss, if the difference between your original purchase price and your future sale price is greater than $250K (if single) or $500K (if married filing jointly) you will be subject to capital gains taxes. These are federal (and in some states, also state) taxes on the "profit" of your home sale.

Read that again: Because of interest and property taxes, you could sell your home at a loss and still be taxed on the “profit”.

Aligre Insight: Unless you are purchasing a home cash, or have such a large downpayment that the interest charges don’t outpace appreciation: It is not a good time to buy a home.

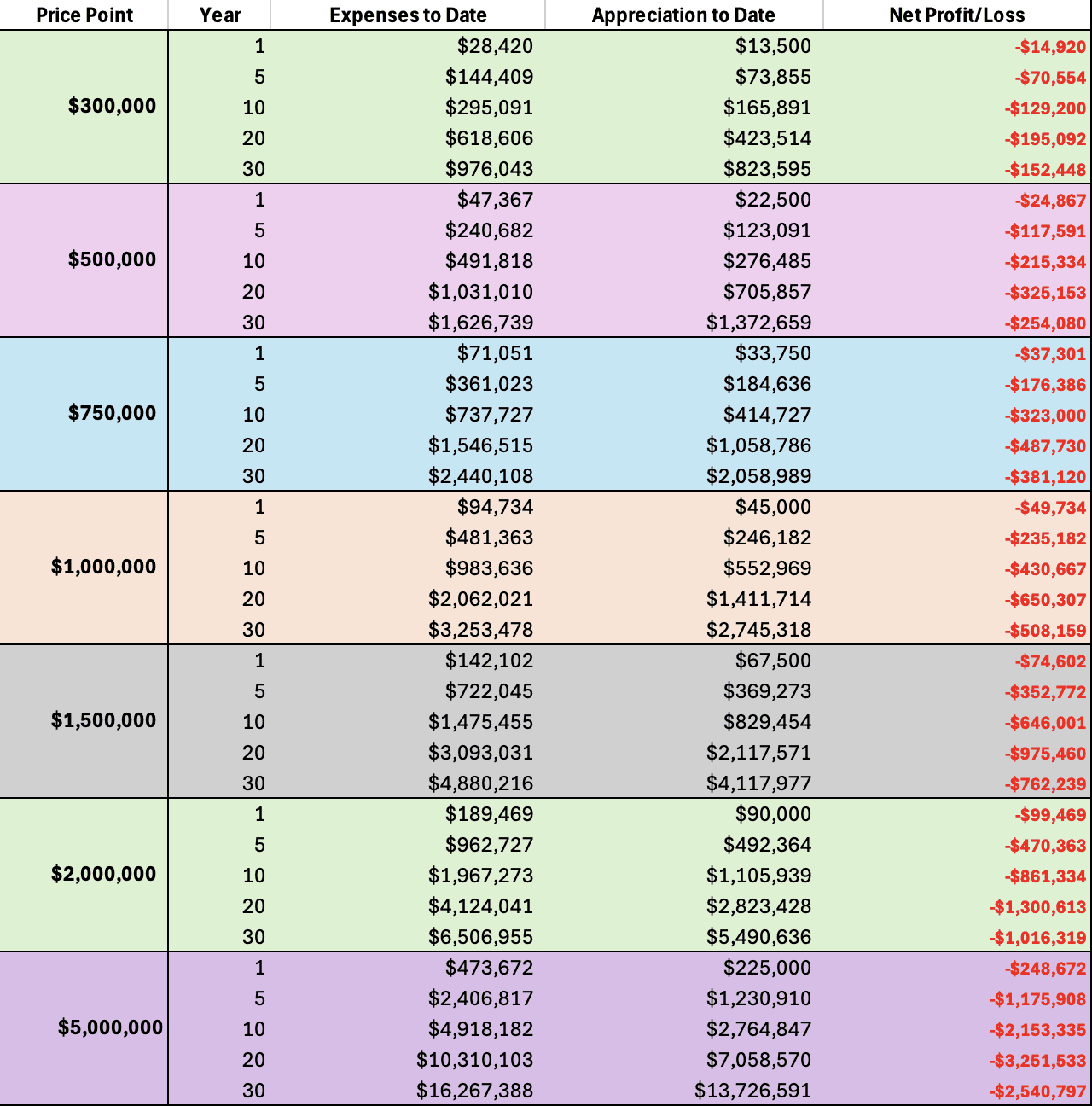

Below is a table showing 7 different price points ($300K on up to $5M) and our profit/loss projections for each price point at 1,5,10,20 and 30 year intervals. You will see that at interest rates in the low to mid 6s, and with a 20% down payment each price point will lose money for the home owner due to the high cost of ownership.

This does not change based on location, with the exception that areas with high appreciation will yield higher home values that could change these projections. Based on historical appreciation rates however, none of these price points will make the owner a net profit within 30 years.

The Core Signals That Define the Best Time to Buy a House

Will the home achieve a net profit in the timeframe you plan on owning it? This is the most important question when deciding "Is it a good time to buy?" and one that can be answered by several factors:

1) What your annual cost of ownership will be

2) What your annual appreciation rate will be

3) How long you plan on spending in the home

How much a home may go up in value is only a part of the story when deciding "is it a good time to buy?"

You will spend money owning the home each year, and this amount should be subtracted from the amount the home goes up to determine your net profit. The answer of "Is it a good time to buy?" depends largely on how much net profit you expect, need or want to make.

Determining Annual Cost of Ownership:

Each year you will spend money on expenses that don't directly increase your homes value, or make you money. Those things are:

1) Mortgage Interest

2) Property Taxes:

3) Insurance

4) Maintenance & Repairs

To figure out how much interest you might pay, you can use online tools like amortisation calculators (it will show the interest you will pay each year) or you can ask a lender to show you that number. The interest you will pay is going to be the largest "cost of ownership" expense you have so it's essential you know what this is.

Property taxes will be roughly 1% of the homes appraised value, but you should and can look this up online by simply googling "property tax rate in ________". Then multiply this number by the market value. This is a rough approximation, but will give you a good idea.

Your lender can also help project this. You can use Grok or ChatGPT to give you an idea of insurance rates in the zip code and property value you are considering, and you can also assume 1-4% of the homes value will be spent on maintenance and repairs each year. Once you have all of these numbers, add them up to get your total cost of ownership.

Determining your annual appreciation rate

The simplest way to anticipate how much a potential purchase will go up in value, is to ask ChatGPT (or Grok) "Annual appreciation rate for XYZ zip code". Historical averages are around 4.5%. You can then multiply the home value by this number to get a projected appreciation value for year 1.

For example, if you were thinking of buying a home that is $100,000 today, and it had an appreciation of 4.5%, it means that home would be worth $104,500 in roughly a year. If your cost of ownership was less than $4,500 than your home had a net profit in year 1, which is pretty darn good. Keep reading to learn more about how time plays into all of this.

Time & it's impact on "Is it a good time to buy a home?"

When deciding if it's a good time to buy a home, you care about how much it will cost you to own the home, against how much the home goes up in value. If it goes up in value more than it costs you to own it, it's a good investment. If it costs you more to own it than it goes up in value, that's probably a bad investment.

However, just because a home doesn't make a "net profit" in year 1 doesn't mean it's a bad investment. The reason for this is, you only really need the home to make a "net profit" at some point before you decide to sell it.

Put another way: If you pay $30,000 in interest in year 1 of home ownership, you ideally will want the property to appreciate at least $30,001, otherwise you will have actually lost money by owning the home. The good news is, you likely aren’t planning on selling the home 1 year after purchasing it so if you aren’t “profitable” after the first year, that’s perfectly okay (and very normal) because you don’t actually lose money until you sell. BUT- you want to be paying attention.

Your goal is that by the time you plan to sell (if you have a timeline in mind when you make the purchase) your home will have appreciated more than it is cost you to own it.

Decide for Yourself

One exercise you can do is to imagine how long you will own the home (let’s pretend it’s 5 years) and then do a comparison of what it will cost you to own that home for 5 years, versus how much the home will go up in value over 5 years.

If you pay $30K in interest each year, you will have paid $150K in interest over 5 years. If the home has gone up $90K in value, this means you will have paid $150K in interest, to get $90k in appreciation. You will have actually lost $60K owning the home, even though it looks like you made a $90K profit.

The best thing to do is estimate your expected time in the home, and estimate how much you will spend owning it each year (using the math above) with how much it may go up in value (again using the math above) and subtract the expenses from the projected value.

Aligre Insight: If the home goes up more than you spent owning it, that is a good investment and would indicate: yes, it's a good time to buy a home. If the home costs more to own than it goes up in value, we would say: no it's not a good investment and it's not a good time to buy a home.

We hope this helps and if you have questions, please e-mail us at hello@aligre.com!

Signup to Aligre

Popular Posts

Oct 29, 2025

"When is the best time to sell?" is a question that 90% of sellers ask. However, the question that has to be asked is, "When is the appropriate time for me?"

Read More

Read More